Start your SIP today and let your money work for you. Systematic Investment Plans help you build wealth gradually, discipline your savings, and secure your financial future.

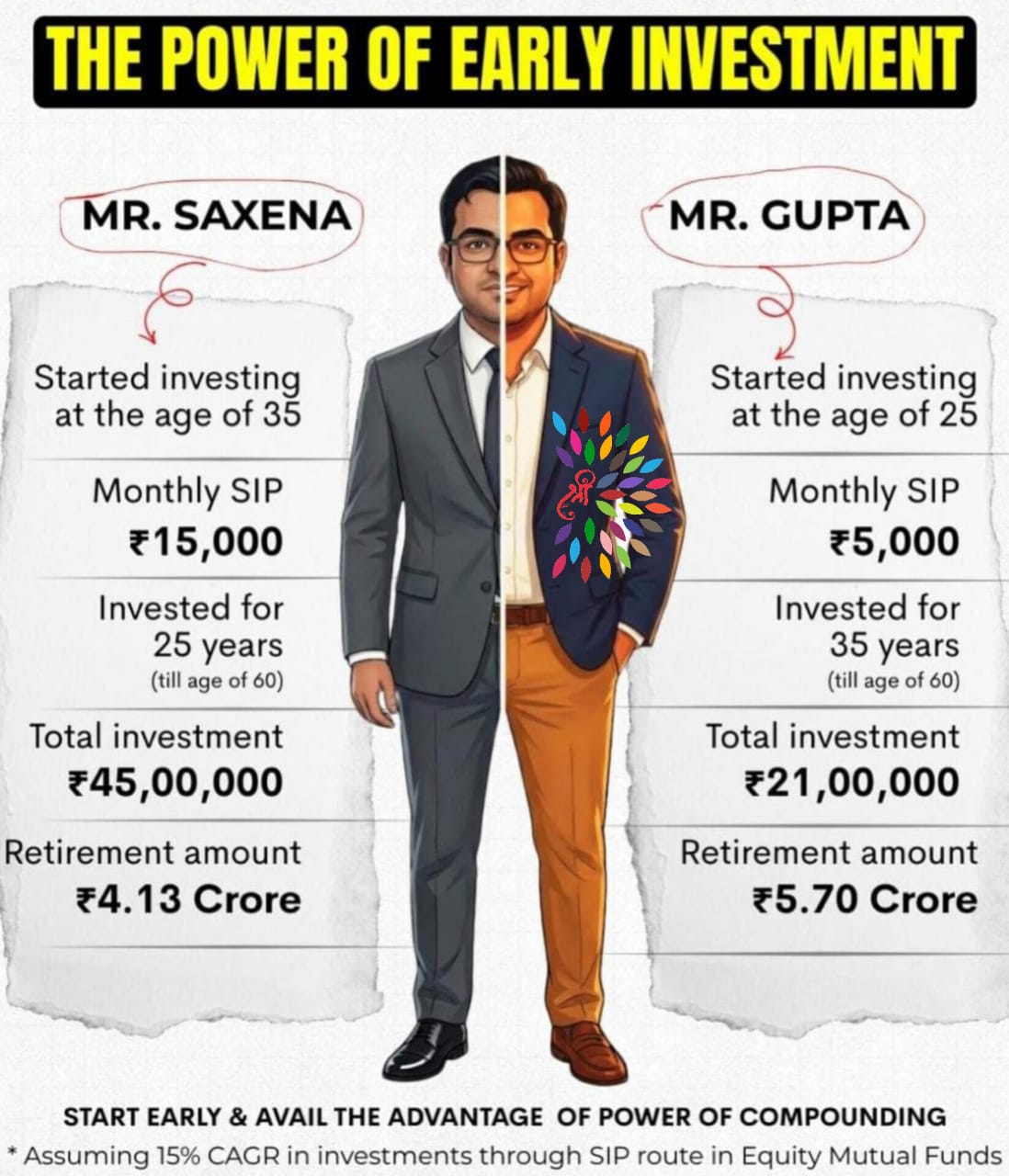

Early investment is one of the most powerful tools for wealth creation.

As shown in the image, an investor who starts investing early can create

significantly more wealth in the long term, even with a smaller amount.

Through a Systematic Investment Plan (SIP), you can invest with discipline

and take maximum advantage of the power of compounding.

Start your investment journey with Shreejeet Wealth today and secure your

financial future.

A Systematic Investment Plan (SIP) is a simple and effective way to create

wealth over the long term.

Through regular investments, you can benefit from market ups and downs

and steadily grow your savings with the power of compounding.

With the guidance of Shreejeet Wealth, you can achieve your financial goals—whether

it’s retirement, your child’s education, or overall wealth creation—in a

planned and disciplined manner.

Start investing today and build a financially strong future for tomorrow.

Strong market momentum combined with the right investment strategy can take

your wealth to the next level.

Equity and growth-oriented investments are powerful sources of long-term

capital appreciation—especially when decisions are made with expert guidance.

With Shreejeet Wealth, you can maximize market opportunities while balancing

risk and confidently moving toward your financial goals.

Smart planning today lays the foundation for strong wealth tomorrow.

Bigger dreams need bigger planning and expert guidance.

Personalized investment strategies designed to grow and preserve your wealth over time. Through disciplined investing, asset allocation, and periodic reviews, we help you achieve long-term financial growth aligned with your life goals.

Goal-based financial planning that helps you manage income, expenses, and savings efficiently. Whether it is buying a home, planning a vacation, or achieving lifestyle milestones, structured planning keeps you financially prepared.

A detailed assessment of your risk tolerance, financial situation, and investment horizon. Risk profiling ensures that your investments are aligned with your comfort level, helping you make informed and confident financial decisions.

Professional portfolio management to balance risk and returns across different asset classes. We continuously monitor, rebalance, and optimize your investments to keep them aligned with changing market conditions and personal goals.

Planning and building an emergency fund to handle unexpected financial situations such as medical emergencies, job loss, or urgent expenses. This ensures financial stability without disturbing your long-term investments.

Comprehensive risk management solutions to protect your financial future. Through insurance planning and diversification strategies, we help safeguard your wealth against unforeseen risks and uncertainties.

Years of Experience

Happy Families

Investors

Mutual Fund Schemes

Introduction Disciplined investing is essential for building wealth steadily over time. It involves consistently allocating funds toward investments, regardless of...

Read More

Every November, as we celebrate Children's Day, we honour the innocence, joy, and limitless potential of childhood. Parents buy gifts,...

Read More

Midcap funds have always been popular with retail investors. Its popularity has only grown further in recent years with midcap...

Read More

"I am extremely satisfied with the guidance and expertise provided by "Shreejeet wealth" team. The investment advice is clear, transparent, and perfectly aligned with my financial goals. Thanks to their strategic mutual fund recommendations, my portfolio has shown consistent growth. I truly appreciate the patience, professionalism, and personalized attention throughout the process."

I have had very cordial relations. Due to my total ignorance about financial market, I keep bothering Shreejeet Wealth team off and on but they has been always very kind in solving my queries. I wish them good luck!!

Investing feels simple... Good fund selection

Very helping and cooperative in all related work.

Shreejeet wealth provides outstanding service. They helped me build a solid financial plan. Their clear communication and personalized approach give me great confidence in my investments. Highly recommended.

Great advisor for years! Learnt a lot from Shreejeet Wealth.

Best financial advisor

Best advises with frequent alerts for higher returns.

I have been associated with Shreejeet Wealth for more than three years, and they have managed my investments with great professionalism. The team is always supportive, patient in resolving doubts, and proactive in sharing market insights. Their strong market knowledge and clear communication make investment decisions easier to understand. I truly value their honest guidance, consistency, and commitment to long-term financial growth.

Very good experience & cover my all loses after i connect with Shreejeet Wealth.

'Guidance like a Father'- I started my investing journey as Amateur in financial market but Shreejeet Wealth guidance acted like a father-providing disciplined direction, timely advice, and a strong foundation for long-term wealth creation.

Professional, transparent, and genuinely focused on client goals—excellent guidance at every step.

"Shreejeet wealth" is a very fine concern for investments in MFs and other savings portfolios. With patience one can achieve targets.

I have been a client of Shreejeet wealth for over five years and their expert guidance has transformed my investment journey. In a volatile market, they provided timely advice on stock selections and portfolio diversification, helping me achieve consistent returns above benchmarks while minimizing risks suitable for my age and health-conscious lifestyle. What stands out is their personalized approach-they take time to understand my goals, explain complex market trends simply, and ensure transparency in every decision. Thanks to their support, I've built a secure portfolio that aligns with my long-term financial needs. I wholeheartedly recommend Shreejeet Wealth to anyone seeking reliable, ethical investment advice in Jaipur or beyond.

Shreejeet Wealth has been instrumental in structuring and strengthening my investment journey from the very beginning. I sincerely appreciate the firm’s professional approach, deep market understanding, and client-first philosophy. Starting with a modest investment, I was guided step-by-step through every stage of the process. The team ensured complete clarity on investment fundamentals, risk assessment, and portfolio construction, effectively hand-holding me through each decision with precision and confidence. With their disciplined strategy, transparent communication, and continuous monitoring, I have successfully built a well-aligned and goal-oriented portfolio. Shreejeet Wealth stands out for its commitment to long-term wealth creation, ethical advisory, and structured guidance. I would highly recommend their services to anyone seeking professionally managed, reliable, and growth-focused investment solutions.

I have a smooth and reliable experience working with Shreejeet Wealth for managing my SIP records. They maintain clear and well-organized records and help with all my investment -related queries whenever needed. Their work is transparent, dependable, and professional.

"I started investing in mutual funds due to only friendship relation with Shreejeet Wealth, since then my portfolio management has been smooth and worry free. The support team has been quite helpful in answering my queries, very fast n quick responsive, always soft spoken. Every time available to help for any query. I must say 24/7. I have so far loved the journey with them and hope to do so for many years to come. Good Work Shreejeet Wealth team."

"Shreejeet Wealth has helped me a lot in my investment plans and managing my portfolio. They have been very helpful throughout this journey. I am very thankful to them for helping me through. I began my journey with a modest investment, and with their well-structured, tailor-made strategies and continuous support, I have gradually built a disciplined and diversified portfolio. Shreejeet Wealth's easy user interface is an added asset for tracking my portfolio, It was difficult for me to understand these plans all by myself, they made me understand these aspects very efficiently. A big Thanks to Shreejeet Wealth."

"I have been associated with Shreejeet Wealth since 2018. They helped me in taking my first step into equity investments. the team has been informative throughout this journey. I had done goal based planning and lined up the portfolio accordingly. Shreejeet Wealth has an easy user interface is an added asset for tracking my portfolio. It was difficult for me to understand these plans all by myself, Thank you Shreejeet Wealth for making it simple for me."

LAYERS

Heading

LAYERS

Heading

LAYERS

Heading

LAYERS

Heading